Why Predictive Modeling Matters in Economics

Truth be told, history has taught us that we cannot simply rely on past and present data as it is and instead need to analyze it to determine what it could spell for our future. And that is because there have been several crises where people had half the information they needed to take the necessary steps to avert the crisis.

Take the 1997 Asian financial crisis, for example. At the time, Thailand, Indonesia, and South Korea had booming economies, and they pegged their local currencies to the US dollar to attract more foreign investors. Domestic banks and corporations that wanted to cash in on this boom started borrowing a lot of cheap short-term cash in US dollars and lending it to locals. But they failed to look at the short-term external debt-to-reserves ratio. After all, if this ratio rose above 1.0, it meant that if foreign lenders suddenly asked for their money, the central bank did not have enough to repay them, which threatened the collapse of their currencies.

So, despite the fact that the ratio had risen above 1.0, local banks and corporations in these countries continued borrowing a lot of money and lending it out locally, believing that the boom would last. Unfortunately, a slight real estate scare in 1997 prompted foreign investors to pull out their money, resulting in Thailand running out of its dollar reserves in only days, plunging millions of people into poverty in a matter of days. Once that happened, investors in Indonesia realized that this country was subject to the same vulnerabilities, and they rushed to convert their Indonesian Rupiah into dollars, resulting in the Rupiah losing over 80% of its value. South Korea was next since its massive conglomerates had also borrowed a lot of foreign currency, and banks had a high number of bad loans. By November 1997, it had run out of reserves and had to sign an IMF bailout amounting to $57 billion.

The 1997 Asian financial crisis is not alone. We have seen several others, including the 2019 Lebanese financial collapse, where the central bank ignored its net foreign exchange reserves, and the 2022 Sri Lankan sovereign default, where the country ran out of money to buy essentials such as food and medicine. There were warning signs, and yet these countries still found themselves in dire situations, all because they did not predict the future accurately.

These and other scenarios show why predictive modeling matters in economics. In a world where timing is everything, economists need the tools to not only understand the past and the present but also predict the future so that they can be proactive rather than reactive. Let us take a look at how these models play a part in shaping policies and mitigating economic risks, while also highlighting the main trends they explore and the top approaches used as of today.

Which Economic Trends Are Most Studied?

While there are many economic aspects that deserve our full attention, you find that governments, corporations, and other stakeholders often set their sights on the following key trends:

Inflation Rates

Even people who do not understand much about the ins and outs of the economy know that high inflation is a bad thing. After all, anytime that prices go up, they are told that this is the result of rising inflation. And so, from a baseline point of view, they know that it affects the purchasing power of their money.

While a gradual rate of inflation is considered part of economic growth, fast rates result in money losing its value quickly, and this can destabilize the economy in a relatively short period. But how does this play out?

To start with, consumers are often heavily affected by rising inflation rates as they not only make everyday goods more expensive but also deplete their savings, resulting in a lower standard of living and lower consumption appetite. Businesses, too, feel the effect of these high rates because they end up paying more for inputs and also find themselves dealing with unpredictable profit margins that make business planning difficult. And governments, which are at the helm, have no option but to raise their interest rates when inflation rises, which puts a damper on economic growth.

Given the likely effects of inflation, it is important to review the current and past rates and use that same data to predict and plan for the economic future.

Gross Domestic Product Growth

The gross domestic product (GDP) serves as a metric with which we can measure a country’s economic health. Based on its trajectory, we can tell whether an economy is growing or is heading towards a recession. And this direction plays an important role in the decisions we make.

Workers, for example, enjoy high GDP growth because it signals more job opportunities and higher wages. But when it starts contracting, they worry that this can lead to layoffs as more businesses close their doors. Investors also take note of this metric because stock markets thrive when GDP goes up and tank when it starts falling. By tracking the GDP, these investors are able to allocate their capital to investments that promise them a good rate of return.

These are but examples of stakeholders who take note of GDP growth. Others include businesses and the government, whose decisions must reflect the economic reality.

Unemployment Rates

The rate of unemployment in a given region does not just point to its economic health but also to the social well-being of its residents. With this metric, stakeholders can assess various factors, such as the state of the labor market and consumer purchasing power, which can inform their decisions.

For instance, if a region releases a report that shows its unemployment rate is on the rise, this serves as a point of concern for the public. People see this as a sign that job insecurity is increasing, and it is time for them to cut back on spending to prepare for harsh economic times. Governments look at this same metric to determine what social safety nets they need to have in place. Say, for example, that the rate of unemployment has risen for two years in a row. The policymakers would need to look into ways to handle this, such as funding social projects or reducing taxes to help people weather this economic period.

Consumer Spending

The GDP of a country heavily hinges on consumer spending. In fact, in many developed nations, consumer spending accounts for 60% to 70% of the GDP because this spending injects money into the economy, which ends up in businesses and other households. Because of this, stakeholders can gauge the economic health of a country by investigating how confident its citizens are in spending and saving.

Let us use manufacturers and retailers, for example. If predictive reports indicate that consumer spending is about to fall, they can respond by reducing their inventory and stalling any plans to expand so as to avoid the risk of dead stock. Lenders and banks, too, rely on such reports to determine how to handle their clients. If they find that consumer spending is falling, they know that this means that fewer people will take out loans and must thus shift their focus to other models to make money.

Interest Rates

Other than inflation, interest rates are a good way to gauge the state of the economy as they essentially indicate the price of money. If stakeholders have an accurate picture of which way these rates are leaning, then they can understand whether they should gravitate towards borrowing, investing, or saving money.

Homeowners and buyers especially pay attention to these interest rates as they affect their mortgage rates. For instance, if a report indicates that the interest rates are set to rise in a few months, a prospective homebuyer may choose to lock in a mortgage at the current rates instead of waiting, as this will allow them to save money. In the same way, if a corporation comes across a report signaling a rise in interest rates, its management is likely to hold off on making any big investments as the rise will increase the cost of corporate debt.

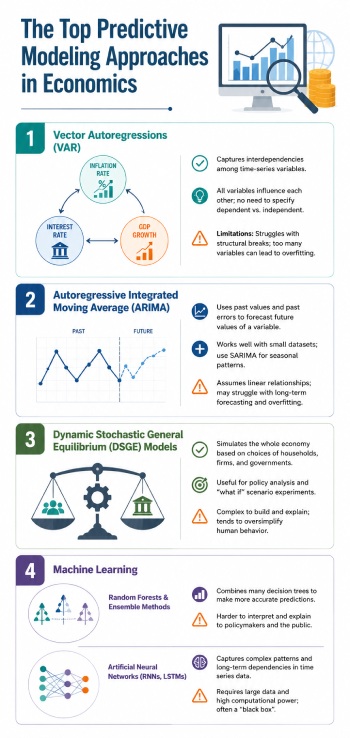

The Top Predictive Modeling Approaches in Economics

In previous years, economists heavily relied on traditional statistical methods to analyze data for the purposes of prediction. But now, thanks to emerging developments in predictive modeling, they have access to a mix of modern tools as well. Let’s take a look at their preferred options:

Vector Autoregressions

This method, abbreviated as VAR, is able to capture the interdependencies that exist among time-series variables. As such, economists love using it when analyzing trends like inflation rates and GDP growth, where variables tend to affect each other. For example, inflation has an impact on interest rates, which then affects the GDP. Given that all these variables have existing relationships, VAR enables economists to create a model where every variable has an equation that explains its own evolution based on its own lags while accounting for the lags of all the other variables within the system.

Thanks to this, VAR is considered highly flexible as it does not require economists to specify the variables that are independent and those that are dependent, seeing as they all influence each other. However, it is important to note that this approach is not effective at handling sudden structural breaks such as pandemics or sudden wars. Moreover, where economists add too many variables, they could face the curse of dimensionality, which would cause data sparsity.

Autoregressive Integrated Moving Average (ARIMA)

This univariate time series model enables economists to smooth out trends (integration) and predict the future values of variables based on their own past values and past forecast errors, hence the terms autoregressive and moving average. Therefore, it is often used in predicting trends such as unemployment rates and inflation rates in the short term.

On the upside, it requires very little data besides the timeline of the variable being studied. For example, if an economist wants to predict unemployment rates in New York, they could use anything from 5 to 10 years of monthly or weekly data to build their baseline. What’s more, while ARIMA can only model trends in non-seasonal time series data, economists have the option to use SARIMA, which can capture seasonal patterns, such as seasonal spikes with predictable and repeating cycles.

While ARIMA comes with various perks, it has the disadvantage of assuming linear relationships and can struggle with long-term forecasting because its predictions lack the capacity to project unexpected structural changes. SARIMA also runs the risk of overfitting the data in long-term forecasting because this model comprises a large number of parameters.

Dynamic Stochastic General Equilibrium Models

These models simulate how the whole economy behaves by modeling the choices that individual households, businesses, and governments make under conditions of uncertainty, such as policy changes and technology shifts. As such, they are best suited for predicting GDP growth and analyzing the impact of interest rate policy changes by central banks. Since they are heavily rooted in economic theories, they can be effective in simulating the long-term effects of policies. To add to this, they provide a framework that researchers and economists can use to run experiments in the “what if” category and thus excel at simulating how unpredictable events can affect the economy.

However, these models are very difficult to build, and they tend to be mathematically rigid, which makes it hard to explain their workings to the general public and policymakers. Furthermore, they tend to oversimplify human behaviors for the purpose of math.

Machine Learning

Economists have come to rely on random forests and ensemble methods as well as artificial neural networks, which are both forms of machine learning.

Random Forests and Ensemble Methods

This approach builds decision trees such that each tree gives its own prediction based on a subset of data features, and the model averages the results of these trees to make a decision. This non-linear approach makes them suitable when analyzing large datasets, such as when investigating consumer spending or the volatility of financial markets, because these models are able to capture complex non-linear relationships between variables that traditional models would miss.

But this same uniqueness serves as a barrier when it comes to justifying the predictions. Since analysts cannot track how all the trees interacted to reach a specific prediction, nor can they extract a simple formula to explain how one input changes the output, policymakers may have a hard time explaining their rationale to the public.

Artificial Neural Networks

More recently, economists have turned to advanced machine learning algorithms that have been inspired by the human brain. At present, the top options are recurrent neural networks (RNNs) and long short-term memory (LSTMs). Unlike RNNs, which have a single repeating layer that makes them lose context during longer sequences, LSTMs feature a complex repeating module that enables them to store information across long sequences. So, while RNNs are best for short sequences that require immediate context, economists can use LSTMs for time series forecasting in the long term, which makes them ideal for predicting financial markets and interest rates.

As a whole, these artificial neural networks offer unmatched power in predicting patterns in highly volatile and complex environments compared to their traditional counterparts. However, economists must use caution with these models as they can memorize historical patterns rather than understand them, which can lead to overfitting.